The Standard Nobody Talks About (But Should)

Let’s be honest. When insurance professionals hear “IFRS implementation,” their minds immediately jump to IFRS 17. And rightfully so – it’s the most significant change in insurance accounting in decades. But in that shadow, another standard quietly reshapes balance sheets across the industry: IFRS 16, Leases.

Here’s the thing: insurance companies have significant lessees. Think about it – all those branch offices where customers walk in to file claims, the fleet of vehicles for claims adjusters, the IT infrastructure humming in data centers. These aren’t trivial amounts. And yet, IFRS 16 is often treated as a “technical exercise” – something the accounting team handles while the real action happens under IFRS 17.

This article is for CFOs, actuaries, regulators, and auditors who want to understand how these two standards interact – and why getting this right matters more than you might think.

The Timing Paradox: Where Balkan Insurers Stand

For insurers in the Balkan region, there’s an interesting timing situation. IFRS 16 has been live since 2019 – it’s already embedded in your financial statements. But IFRS 17? That’s still 2-3 years away for most. Slovenia and Croatia have already made the jump, but for everyone else, IFRS 4 remains the current reality.

This creates what I call the “preview window” – a period where you’re already living with IFRS 16 while preparing for IFRS 17. Smart insurers use this window to think ahead. The interactions between these standards aren’t obvious, and discovering them during your IFRS 17 transition sprint is… let’s just say, not ideal.

IFRS 16 Through an Insurer’s Lens

Before diving into interactions, let’s ground ourselves in what IFRS 16 actually does. The core principle is elegantly simple: if you have the right to use an asset for a period of time, that right has value – and that value belongs on your balance sheet.

Gone are the days of operating leases hiding in footnotes. Under IFRS 16, lessees recognize a right-of-use (ROU) asset and a corresponding lease liability for virtually all leases. The income statement sees depreciation on the ROU asset and interest expense on the liability, replacing the straight-line rental expense of the old world.

What Does a Typical Insurance Lease Portfolio Look Like?

Non-life insurers typically have extensive lease portfolios. Picture a company with 50 branch offices spread across the country, each with a 5–7-year lease. Add 30 vehicles for claims adjusters. Throw in IT equipment – servers, laptops, specialized scanning equipment for document processing. The numbers add up quickly.

Life insurers often have fewer leases but larger individual values – think headquarters buildings and regional offices rather than widespread branch networks.

One quirk that catches insurers: the incremental borrowing rate (IBR). Unlike manufacturing companies that regularly borrow for equipment, many insurers don’t have obvious market borrowing rates to reference. Determining an appropriate IBR requires more judgment, and auditors will ask questions.

The Current State: IFRS 16 Meets IFRS 4

If you’re still on IFRS 4, your balance sheet has already absorbed IFRS 16. ROU assets typically sit within property, plant, and equipment (or, in certain real estate leases, investment property). Lease liabilities appear among other financial liabilities. The income statement shows depreciation and interest rather than rental expense.

For most insurers, the IFRS 16 transition was… unremarkable. A technical adjustment, some new disclosures, perhaps some covenant discussions with lenders. The “insurance” side of the business continued under IFRS 4 as if nothing had happened.

This perception of IFRS 16 as a “non-event” is about to change.

Enter IFRS 17: Where Things Get Interesting

IFRS 17 fundamentally changes how insurance contract economics flow through financial statements. It introduces concepts like fulfillment cash flows, the contractual service margin (CSM), and a new expense classification distinguishing insurance service expenses from insurance finance expenses.

Here’s where IFRS 16 enters the conversation: Are costs associated with leased assets “directly attributable” to insurance contracts?

This isn’t an academic question. Under IFRS 17, costs that are directly attributable to acquiring or fulfilling insurance contracts affect the measurement of insurance contract liabilities – and potentially the CSM. Costs that aren’t directly attributable remain as other operating expenses.

The CSM Connection

Consider a simple example. Your claims department operates from leased premises. Claim handlers use leased vehicles to conduct inspections. Under IFRS 4, you recorded rent expense and vehicle lease expense as operating costs – straightforward.

Under IFRS 17, you need to determine whether depreciation on these ROU assets is part of the fulfillment cash flows. If the claims handling activity is directly attributable to fulfilling insurance contracts (which it typically is), then the related costs – including ROU asset depreciation – may need to be included in your fulfillment cash flow estimates.

The same logic applies to acquisition activities. Sales agents operating from leased branch offices, using leased laptops to complete applications – if these costs are directly attributable to acquiring insurance contracts, they flow into your acquisition cost attribution under IFRS 17.

The New Expense Split

IFRS 17 creates a cleaner separation between insurance service results and finance results. Under IFRS 16, your lease costs are already split between depreciation (operating) and interest (finance). Under IFRS 17, you need to think about where each component lands:

ROU asset depreciation related to insurance activities → potentially part of insurance service expenses. Lease liability interest → remains in finance costs, separate from insurance finance income/expenses. This isn’t just a presentation – it affects how investors and analysts understand your operating performance versus financing decisions.

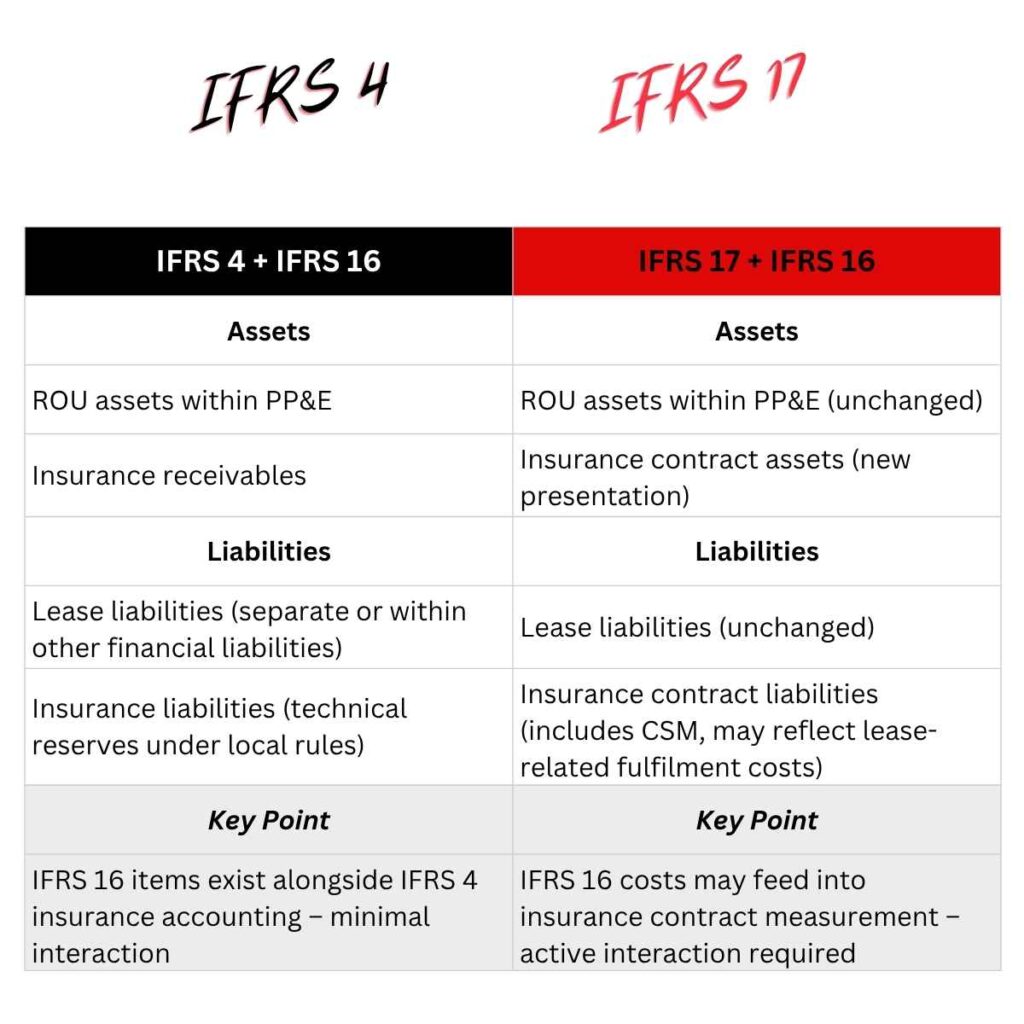

Balance Sheet Face-Off: Before and After IFRS 17

Let’s look at how your balance sheet evolves. The table below shows the conceptual shift – not in the IFRS 16 items themselves (those stay consistent), but in how they interact with the insurance contract presentation.

The fundamental insight: under IFRS 4, your lease accounting and insurance accounting lived relatively separate lives. Under IFRS 17, they need to talk to each other.

Solvency II: The Regulatory Overlay

For European insurers (and those following similar frameworks), Solvency II adds another dimension. Your regulatory balance sheet isn’t your IFRS balance sheet – but changes in one affect the other.

ROU assets and lease liabilities flow into your Solvency II balance sheet. The treatment isn’t always intuitive. ROU assets are generally valued at their IFRS carrying amount for Solvency II purposes (with some exceptions for property). Lease liabilities typically receive similar treatment.

The impact on Own Funds depends on the net position, and since ROU assets typically depreciate faster than lease liabilities decline in early years, the effect on regulatory capital can be negative initially.

When IFRS 17 arrives, you face a double transition in your regulatory reporting: new insurance contract measurement affecting technical provisions, and potentially revised treatment of costs flowing through those calculations. Regulators like NBS and ASO are watching – even if IFRS 17 isn’t mandatory yet in their jurisdictions, they’re aware it’s coming.

Practical Pitfalls: What Catches People

The “hidden leases” discovery. Many insurers discovered leases during IFRS 17 implementation that somehow escaped IFRS 16 scrutiny. That IT outsourcing contract? Contains embedded leases for dedicated servers. The managed print services agreement? Probably includes equipment leases. The fleet management arrangement? Worth a second look. IFRS 17 projects often include broader-scope reviews that surface these items.

Discount rate confusion. IFRS 16 uses the lessee’s incremental borrowing rate. IFRS 17 uses rates reflecting the characteristics of the insurance contracts. These aren’t the same thing. Don’t assume the methodology developed for one applies to the other.

Modification accounting headaches. Insurance companies restructure constantly – branch consolidations, lease renegotiations, relocations. Each modification under IFRS 16 requires remeasurement. If those modified leases relate to activities included in your IFRS 17 cash flows, you need processes to consistently capture changes.

Intercompany leases in groups. Insurance groups often have property companies that lease to operating entities. At the consolidated level, these eliminate – but at the legal entity level (relevant for regulatory reporting), they create real IFRS 16 balances that need proper treatment.

Lessons from Early Adopters

Insurers in Slovenia and Croatia transitioned to IFRS 17 in 2023. Their experience with the IFRS 16 intersection offers valuable lessons.

Lesson 1: Cost attribution takes longer than expected. Determining which costs are “directly attributable” involves significant judgment and cross-functional discussion. Actuaries, accountants, and operations teams often have different views. Start these conversations early.

Lesson 2: Systems integration isn’t trivial. If ROU asset depreciation flows into fulfilment cash flows, your lease accounting subledger needs to communicate with your IFRS 17 calculation engine. This interface doesn’t exist out of the box – it requires design and testing.

Lesson 3: Auditors will ask detailed questions. The interaction between IFRS 16 and IFRS 17 is a natural audit focus area. Expect questions about consistency, completeness of cost attribution, and documentation of judgments.

Lesson 4: Don’t leave it until the end. Several insurers reported that IFRS 16 considerations were “late additions” to their IFRS 17 projects. This created rework and timeline pressure. Build it in from the start.

Conclusion: Small Standard, Meaningful Impact

IFRS 16 will never generate the headlines that IFRS 17 does. It’s not going to transform how investors understand your business or fundamentally reshape industry practice. But the interactions between these standards are real, and getting them wrong creates problems that are easier to prevent than to fix.

For insurers still on IFRS 4, this is your preview window. Use it. Review your lease portfolio with IFRS 17 eyes. Think through cost attribution methodology before you’re under implementation pressure. Engage your actuaries and accountants in joint discussions now.

The operational reality is simple: leases are part of delivering insurance services. The accounting should reflect that reality – coherently, consistently, and without surprises.

This post is also available in: